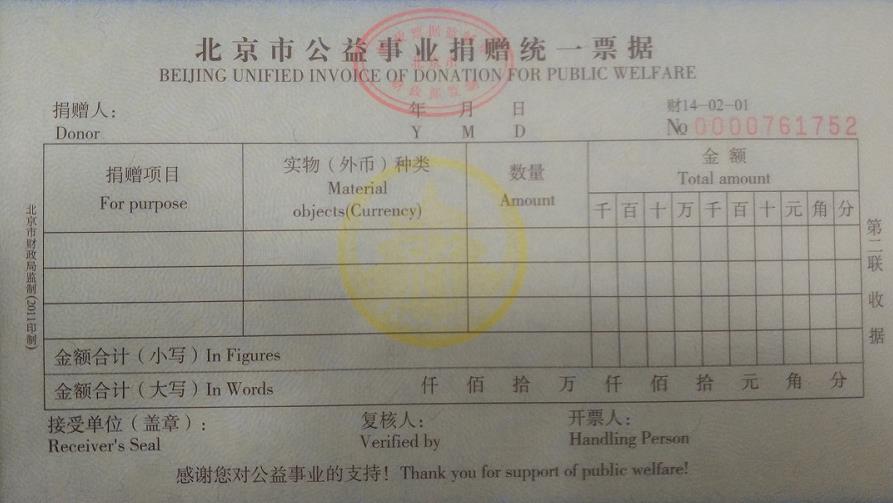

Beijing UFCH Eligible for Pre-tax Deductions for Donations

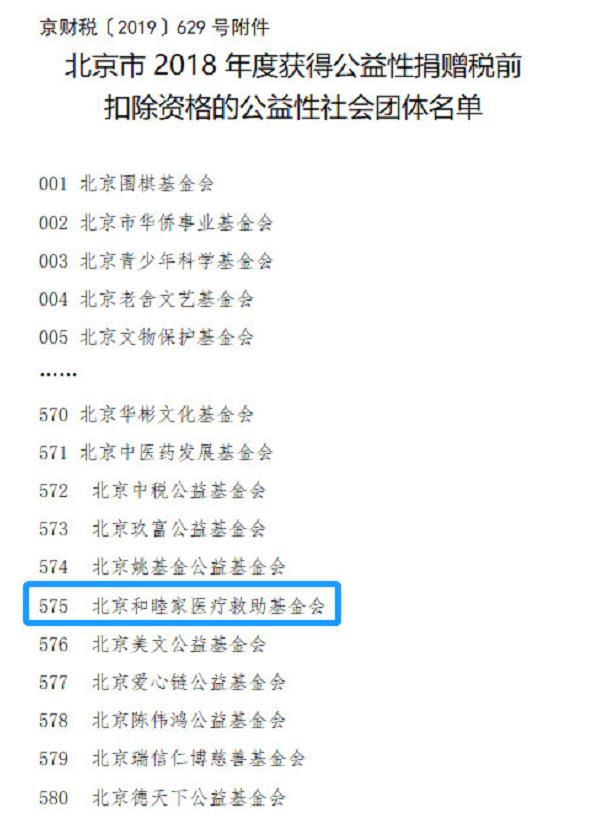

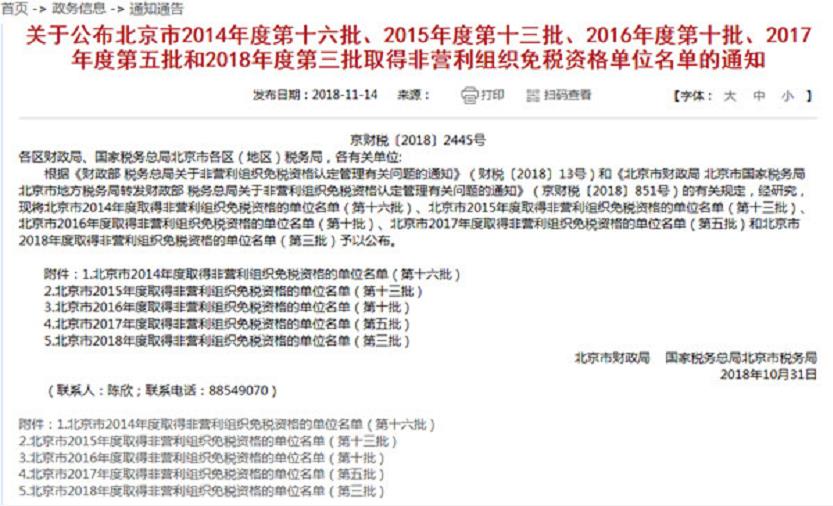

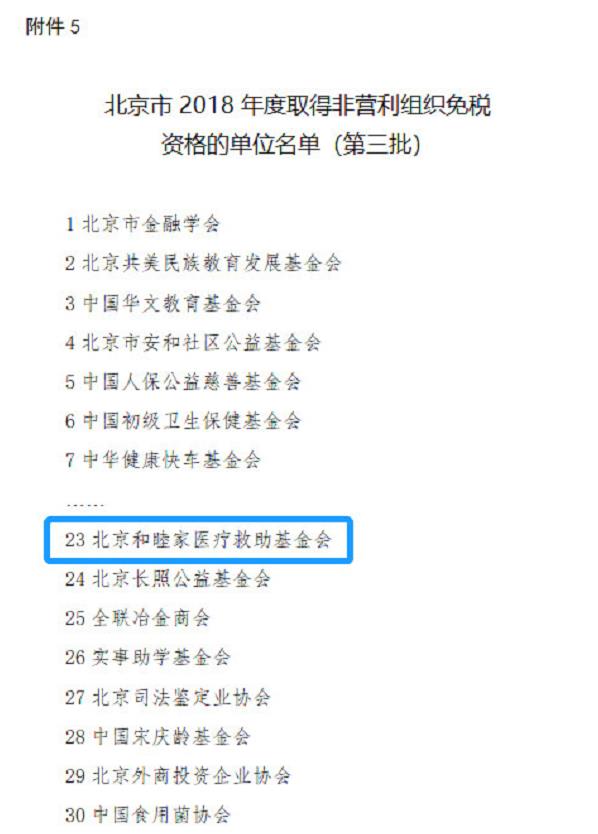

In April, 2019, Beijing Municipal Bureau of Finance, Beijing MunicipalTax Service of State Taxation Administration and Beijing Municipal Bureau of Civil Affairs jointly announced (Document No. 629 [2019] Beijing Finance and Tax) that Beijing United Foundation for China’s Health (Beijing UFCH) will begranted the qualification for the pre-tax deductions for public welfare donations in 2018. Enterprises and individuals that donate to Beijing UFCH to support such projects as “Children’s Medical Care Program”, “Healthcare for All”, “Wheels for Life Mobile Clinic” and “Capacity Building Program” can enjoy the preferential policy of pre-tax deduction of income tax.

The Charity Law of the People’s Republic of China, which came intoeffect on September 1st, 2016, stipulates that natural persons,legal persons and other organizations that donate property for charitableactivities shall enjoy tax incentives according to law. Where an enterprise’scharitable donation expenditure exceeds the amount that is allowed to bededucted in the current year when calculating the taxable income amount of theenterprise income tax as prescribed by law, it is allowed to deduct the amountwhen calculating the taxable income amount within three years after the carry forward.

According to Article 6 of the Individual Income Tax Law of the People’s Republic of China (amended in 2018):

Individuals who donate their income to public welfare and charitable undertakings such as education, poverty alleviation and poverty relief may deduct the portion of their taxable income that does not exceed 30% of the taxable income declared by tax payers. Where the State Council stipulates that donations to public welfare charities shall be deducted in full amount before tax, such provisions shall apply.

According to Article 19 of the Regulations for the Implementation of the Individual Income Tax Law of the People’s Republic of China (amended in2018):

In Paragraph 3, Article 6 of the Individual Income Tax Law, the term “individuals who donate their income to public welfare and charitable undertakings such as education, poverty alleviation and poverty relief” means individuals who donate their income to public welfare and charitable undertakings such as education, poverty alleviation and poverty relief through public welfare social organizations and state organs within the territory of China. The term “taxable income amount” refers to the amount of taxable income before deducting the amount of donation.

According to Article 9 of the Corporate Income Tax Law of the People’s Republic of China (amended in 2018):

The portion of the public welfare donation expenditure incurred by an corporate that is within 12% of the total annual profits is permitted to be deducted when calculating the taxable income amount; and the portionexceeding 12% of the total annual profits is permitted to be deducted when calculating the taxable income within three years after the carryforward.

According to the Notice on the Policies Related to Pre-tax Carryforward and Deduction of Corporate Income Tax for Public Welfare Donations (Document No. 15 [2018] Finance and Tax):

The portion of the donation expenditure incurred by an enterprise for charitable activities and public welfare undertakings through public welfare social organizations, people’s government at or above county-level and its directly affiliated institutions that is within 12% of the total annual profits is permitted to be deducted when calculating the taxable income amount; and the portionexceeding 12% of the total annual profits is permitted to be deducted when calculating the taxable income within three years after the carryforward. The portion of the donation expenditure incurred by the enterprise in the current year or carried forward from previous years that is permitted to be deducted before tax in the current year shall not exceed 12% of the total annual profits of the enterprisein the current year. The portion of the public welfare donation expenditure incurred by the enterprise that is not deducted before tax in the current year is permitted to be carried forward to and deducted in the following years, but the carryforward period shall not exceed 3 years from the following year of the year in which the donation is made. When calculating and deducing the public welfare donation expenditure, enterprise shall deduct the donation expenditure carried forward from previous years first, and then deduct the donation expenditure incurred in the current year.